For government agencies, particularly in the United States, prices for services should be set at a level which is in line with costs. Accurate cost allocation and understanding of cost drivers is critical for this process. Ensure all direct expenses remain within the confines of COGS included in the financial statements. This is important in order to represent the cost that has been incurred by the business in relation to production which is necessary for determining profitability and considering the pricing of products. The right financial reporting software gives you instant visibility into your costs allowing you to put an accurate and efficient cost allocation plan in place. Managers can track expenditures in real time, spot trends quickly, and adjust cost allocations on the fly.

Direct Costs vs. Indirect Costs

In addition, theproportions (Kji) in both sets of equations are different for the same reason. The proportions reflect all of the relationships in the reciprocalmethod, instead of only part of the relationships as in the step-down method. The reciprocal method is more accurate than the other two methods because it fully recognizes self services and reciprocal services between service departments. However, thismethod is more involved because it requires the solution to simultaneous equations.

Time Driven Activity-Based Costing (TDABC)

Cost allocation plays a significant role in a company’s Corporate Social Responsibility (CSR) efforts. Resources, both tangible and intangible, are frequently limited within organizations. The allocation of these resources can either inhibit or promote CSR activities. If CSR is not viewed as a business priority, resources may not be allocated sufficiently to develop and implement effective initiatives. Conversely, if an organization is committed to its CSR responsibilities, it will allocate costs accordingly to ensure its efforts are adequately funded and supported. In summary, the process of cost allocation serves to bridge the gap between operational activities and financial management.

FAR CPA Practice Questions: Capital Account Activity in Pass-through Entities

The various producing departments might use direct labor hours, equivalent units, material costs or machine hours, as an allocation basis. Inthe traditional approach, the activity measures, or allocation bases, are almost always related to production volume (like the four mentioned in the previoussentence). If Product Xconsumes 20 percent of one indirect resource within a department, it must consume 20 percent of all of the indirect resources within the department andthe allocation basis must reflect this percentage. Otherwise a single departmental rate will not provide accurate product costs. Cost allocation methods are essential for distributing indirect costs across various departments, products, or services within a business. One widely used method is the Activity-Based Costing (ABC) approach, which assigns costs based on the activities that drive them.

- In regulated industries such as utilities and telecommunications, companies are often required to allocate costs in specific ways to ensure fair pricing for consumers.

- As indicated in Exhibit 6-14, X1 requires a larger proportion of cutting time, while X2 requires a larger proportion ofassembly time.

- If a firm produces many different products that consumeindirect resources in different proportions, then a two stage approach is needed to provide accurate product costs.

- These are raw materials and supplies that are consumed in the production process and can be directly linked to the final product.

Finally, cost allocation allows companies to compare their performance against similar businesses. The various functional areas within a manufacturing facility are usually separated into two types of departments. These include producing departments and service departments.Producing departments convert raw, or direct materials into finished products. Service departments provide support services to the other departments in theplant.

Teams become accountable for their spending, and you can quickly spot opportunities to reduce waste and improve efficiency. Indirect costs should be allocated between departments, projects, and products based on a fair allocation plan that reflects their use in those areas. For instance, a manufacturing company using varied types of raw materials, labor, and machinery might initially find it difficult to ascertain the price of one finished unit. Cost allocation, however, provides a mechanism to allot each cost element to each unit. Thus, unit costs drive the ultimate pricing decisions and influence the firm’s competitiveness in the market place.

Failure to comply with these regulations can result in fines, penalties, or even legal challenges. Please note that the difference between Time Driven ABC and Rate Based ABC is mainly in the fixed rate within Rate Based ABC. Applying a fixed rate can lead to an over or undercoverage of the total cost of the resource the rate is applied upon. OnEntrepreneur is the go-to source for entrepreneurs looking to get ahead. Our online magazine offers practical, actionable advice to help startups succeed across key areas like business strategy, marketing, technology, leadership, management and more.

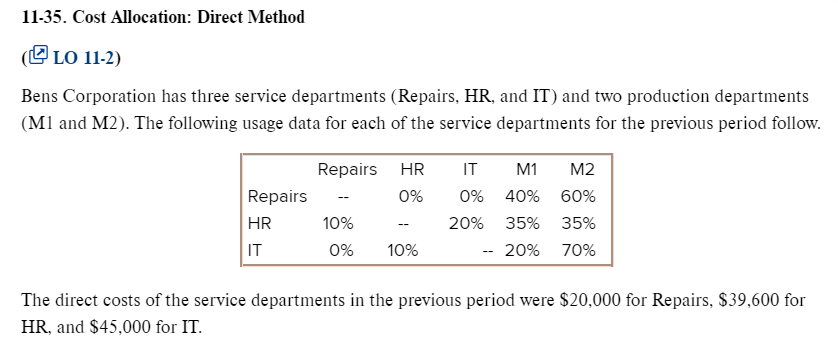

In a real-world setting, the direct allocation method may not fully reflect the true cost of producing a product, as it doesn’t account for the support services provided by departments like HR and IT. Therefore, this method is most suitable for companies with simple, direct production processes and minimal interdepartmental service the standard deduction sharing. Sander den Hartog suggests that organizations shouldn’t wait for perfect data before starting their cost allocation process. Instead, they should begin with the data they have, refine their methods over time, and use the insights gained from initial allocations to improve data collection and cleansing processes.

These expenses are critical for hospitals and clinics to manage, as they directly impact the cost of patient care and the institution’s financial health. This approach ensures that the costs of marketing activities are distributed fairly across the products or departments that benefit from them, rather than being assigned to one area arbitrarily. Manually managing cost allocation can be time-consuming and error-prone, especially for large organizations with multiple cost centers.

This is because cost of goods sold (COGS) is used while calculating gross profit in which case direct expenses adjustment in COGS is important so that profit margin can be gauged properly. Ensure that each expense or cost can be related to or traced back to one specific product or service delivered. This step prevents certain costs that do not directly affect the output from being classified in the direct expense account. Direct labor costs refer to the amount paid to the workforce involved directly in the production process, including salaries and benefits. It includes workers who are involved in the active production of the items or the construction of the structures. Even the best cost allocation system can fail if it’s working with outdated or incomplete data.

The profit impact of using the direct allocation method is relatively minor when your business sells most of its produced goods immediately, rather than retaining them in stock at the end of each reporting period. There are three ways to account for the cost of these service departments, which are noted below. In general, the indirect allocation method requires an excessive amount of accounting work, and so is not recommended. However, the direct allocation method represents a reasonable mix of modest additional clerical work and a more accurate cost allocation.